Posts by David Hood

Last ←Newer Page 1 2 3 4 5 Older→ First

-

Polity: House-buying patterns in Auckland, in reply to

The CPI basket tracks rentals and new houses only- not sales of existing houses. Think of it as the construction materials.

-

Polity: House-buying patterns in Auckland, in reply to

When I looked at it (so up to 2012) I found that immigration was not actually a very good prediction of house prices compared to the arrival of money, and the two did not have very much of a relationship between them.

-

Polity: House-buying patterns in Auckland, in reply to

Basically every young family that has a property in NZ is suddenly worth negative hundreds of thousands of dollars.

It basically means you a never ever moving, so not likely to be ever changing jobs etc.

-

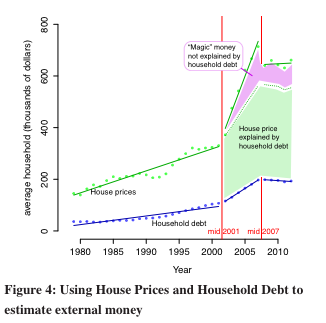

And another graph from around the time- keeping in mind that this is showing 1980-2012 (rather than the early 2000s bubble period of the graph a few pages ago) and being generous with the assumptions about how much could be explained with household debt.

In the accompanying text I wrote, in mid 2013, "And now the worrying bit. The period after 2007 actually fits better if it has the same slope as pre 2002 then has a sudden increase in 2012 (the early 2013 data also supports this). This suggests we may be entering a period of further off-shore money coming in, further pricing out New Zealand households"

-

going back to when I was looking into this in 2013, here is another document, where I was using other numbers that gave similar conclusions, but it is much harder to follow the argument as it is more mathematical.

https://www.dropbox.com/s/tlkq1efejjk0lhv/housepricesanalysis.pdf?dl=0

-

Polity: House-buying patterns in Auckland, in reply to

It was clear during the middle of last decade that ever higher interest rates did little to slow the gain in house prices.

I looked into that too. While interest rates got worse as a predictor of house prices, foreign currency conversions into New Zealand dollars got better as a predictor.

But lets be clear, with regards to interest rate policy and houses, the RBNZ banking stability mandate means it is not actually a problem, provided not too many New Zealanders try and compete by taking out mortgages and buying houses (so that there are not enough mortgages that a downturn destabilises the banking sector). It would lock those with mortgages into a lifetime of "underwater" house value, but provided that number of people is fairly small the banking sector is safe.

Of course, if you believe in quaint fairytale notions of home ownership and community building and social capital... well, that is not the Reserve Bank's mandate, and it doesn't seem to be the present government's interest.

-

Bubble explanations of future gain only really apply in closed model - if you have other drivers like Tony Alexander's one of money hiding- people may be prepared to lose money as "insurance"

-

Polity: House-buying patterns in Auckland, in reply to

It’s just as plausible that the problem is too many people watching Homes Under The Hammer on the Living Channel and deciding to build a property portfolio for their retirement

I can rule that one out- there has been no change in household savings in other forms of wealth or incomes sufficient to account for the rise in house prices.

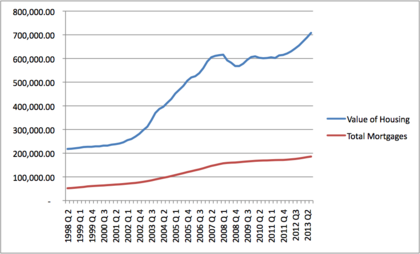

I can tell people exactly what happens if you just talk numbers. You tell people that if you add up the amount of money in mortgages, and the value of NZ housing, it was a rock solid predictable relationship up until 2001/02 then began to diverge in 2001/2002 and that the mystery money cannot be accounted from other sources within the NZ economy (for example household wealth in other forms has not altered, incomes haven't altered, etc). (attached graph)

Then they go "yes, it is a mystery", or rather most of the time "I don't understand". At which point you can't actually say much more as there is no positive evidence of where the mystery money is coming from*, only negative evidence from inside NZ for where it isn't. And the conversation dies as too abstract.

Then you go away and look at other housing markets and establish that in Ireland household debt did go up because Irish people were buying the houses

https://www.dropbox.com/s/gpuhxvs4apfhz7s/bubbles.pdf?dl=0

Then people say "yes, but Ireland was different" so you get the figures for the United States as well, and find that U.S. debt again increased with house prices as local people were buying the houses. Figures at https://sites.google.com/a/thoughtful.net.nz/home/international-house-bubbles

You try and find figures for Australia but their housing market records are even murkier than New Zealands.

At which point those few people still with you go "It is strange isn't it, huh" at which point, because it is clear that the argument is way to technical to get any traction and you have satisfied your own curiosity about the matter, you get on with your own life.

-

Polity: House-buying patterns in Auckland, in reply to

It is that we have what, among New Zealand residents, are two very similiar sized and demographically and socio-economically similar groups both of which can be identified by the proxy of name, so any socio-economic agruments about one group could fit the other (for instance arguments we have seen about age and financial means). However the Indian named population is buying houses exactly in proportion with the proportiion of the self declared ethnically indian in the census. So it is an arguement against the assertion that it is local chinese residents, because (for example) they earn no more than local Indian residents. It is ruling out (or at least making vastly improbable) local cause.

My own personal opinion is that starting from 2001/2002 to 2011 about 30% of price rises must be coming from offshore (initially from Australia)- this is based on the observation that earlier the amount of money in mortgages equals the value of house price rises. After 2001 extra money starts appearing in house value that doesn't seem to be coming from anywhere inside the NZ economy (certainly not residental mortgages). But "this is what happens if you gradually steadily convert residential housing to foreign ownership over a long period of time" makes for a headline that is way to dependent on understanding mathmatical models compared to "you can see the foreign investors acting right now"

-

Regarding the validity of comparing Indian Residents and Chinese Residents. Even without access to Labours internal data, if you go to the census

http://nzdotstat.stats.govt.nz/wbos/Index.aspx?DataSetCode=TABLECODE8021

You can say

- the populations of those that declare themselves ethnically Indian nfd or chinese nfd are about the same

- the number in each population making more than 50000 is about the same (so economically similar for those in a house buying range)

- I've you look at directs of residence, Chinese and Indian correlated better with each other than with New Zealand European (so are living in the same areas at district level)

-Have a pretty similar age profile