Posts by David Hood

Last ←Newer Page 1 2 3 4 5 Older→ First

-

Speaker: House prices and the "Magic Money", in reply to

You’re not comparing apples with apples, you need the $ figures for houses actually sold to compare with the $debt, not the QV valuations.

I don't think you do. The quantum may be different, but the pattern is the same. So for example Figure 2 would show the same lack of relationship for the more recent period. Debt would still explain the same proportion of the pattern, and the relative importance of the unknown component is just as strong on sales.

Other explanations are that NZ calculates total housing value in a completely different radical way to the rest of the world (in which case the NZ economy is toast as our major national asset is worth about 60% of what we have been claiming it is). Or that in the United States and Ireland, in every year everyone in the country has been selling their house to everyone else in the country, so that their total value of houses figures are based completely on prices.

-

Speaker: House prices and the "Magic Money", in reply to

The influence of LGA 2002 on house price rises

IMO the whole LGA arguments people make involve a bit of cognitive dissonance- Not only did prices go up, the amount of debt required to purchase the increased prices went down as a percentage of the price, which is really, really weird if the LGA was the reason.

-

Speaker: House prices and the "Magic Money", in reply to

$300billion

In reality the 300 billion is just an influence figure (not actual cash) and the meta point would be that there is a 3 to 5 influence that needs to be accounted for in any discussion. That is also a 3 to 5 influence across all properties in New Zealand.

-

Speaker: House prices and the "Magic Money", in reply to

But the figure you have for “total house value” is a statistical valuation, right? It’s based on looking at actual sales prices versus a baseline (like GV) and applying that to all the properties.

It is, ...but if you look at the REINZ property sales graph is has the same pattern of rises and falls as the house values one, so without access to the REINZ sales data the similarity of the REINZ graph to the total value graph means that the lack of relationship between values and debt should be reflected in prices. That is an deductive leap in the absence of the actual data, but one I can't see any evidence for not making. I will also point to other countries and say "their numbers add up".

Also, is commercial debt (as in property developers borrowing to “land bank”) counted as household debt?

I don't know (if anyone does have public data getting total bank lending by category that would be handy) but given the "Magic Money" gap has grown to 60% of the "traditional household purchases through mortgages" influence on the entire national housing market in 15 years, I would expect there to secondary evidence inside the NZ economy figures.

-

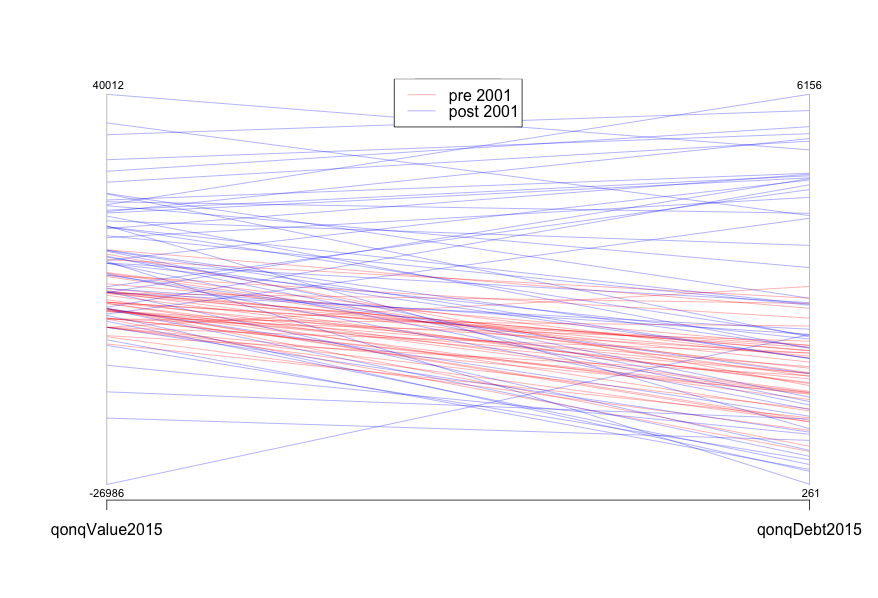

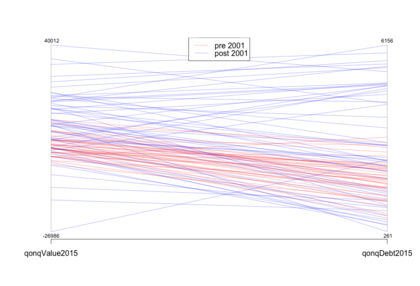

One more graph- I was introduced to parallel coordinate charts this week, for showing the relationship between two variables. this is NZ Quarter on Quarter debt and housing prices. I didn't use it because most people have never seen it before so it can be a bit baffling. But the largely predictable parallel lines for the pre2001 data suggest that there is a tight relationship, the all over the place slopes of the post 2001 data suggests that relationship has weakened dramatically

-

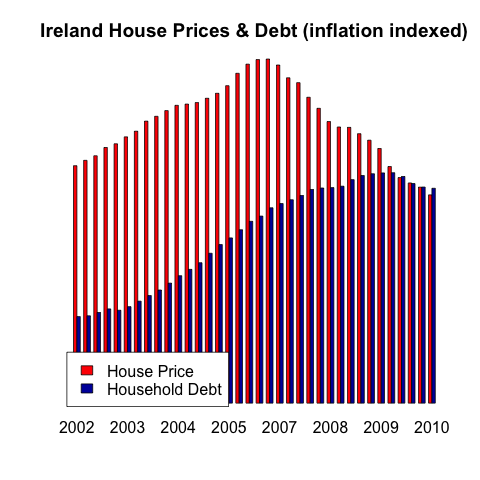

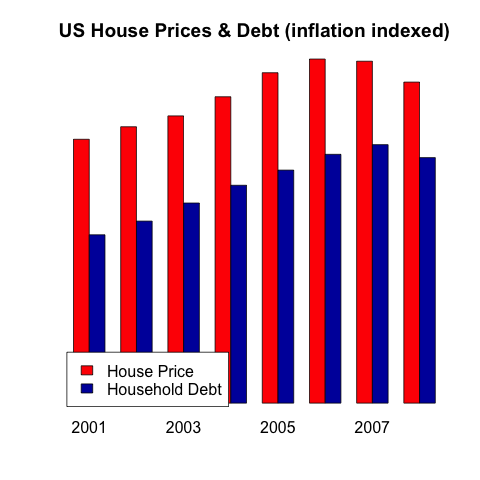

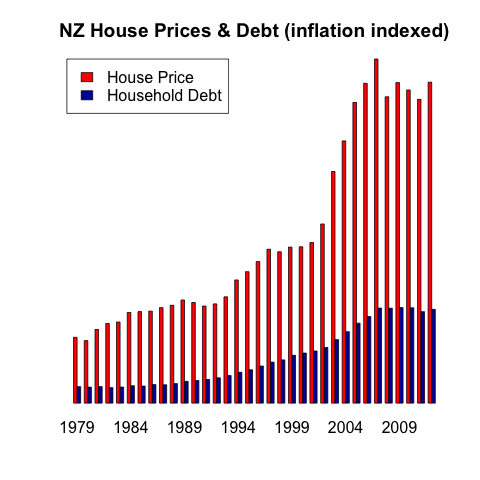

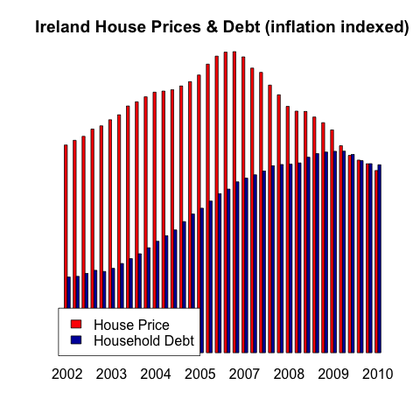

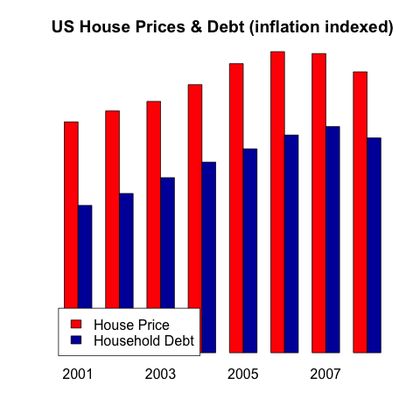

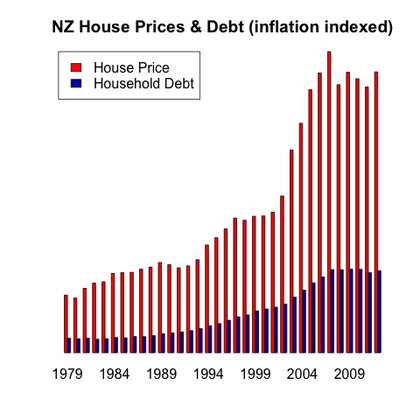

Here are a few other graphs, that didn’t really fit the post focusing on working out the values for New Zealand. Looking at debt in Ireland (internal boom and bust) and the United States (the size of the market means that nationally it is mostly internal buying) you can see the way debt tracked up not only in the same pattern but also by the same amount. The NZ market is different, which suggest applying supply and demand models to it based on a general understanding of housing supply and demand will be wrong.

-

Speaker: House prices and the "Magic Money", in reply to

If you had a country where house sales were very unusual

It might be possible to contract a sufficiently unusual situation to explain it, but it is very hard for those explanations to to leave traces in other parts of the economy- sudden simultaneous remortgaging should affect household debt (since prices are going up). A drying up of property so a smaller sample making the values less meaningful should show up as dramatic changes in sales numbers.

It could all by caused by the unusual market situation of one house that is being sold between people with overseas capital every month doubling each time. And that one house is now worth 256 billion dollars. But that would also leave secondary evidence.

-

Speaker: House prices and the "Magic Money", in reply to

Well spotted, opps.

I updated the github version to

Authority X said it was supply constriction due to RMA restriction. I am sure they did. The RMA came in in 1991 (thanks to Rich of Observations for a correction here) and the LGA (the other main target) came in in 2002 and was implemented in 2003. Either requires a dose of time travel, but neither explain the lack of debt rise. We come back to if around 300 billion in the 800 billion in Housing Value gains is not explanable by inside the economy debt, how many houses do you need to build to satisfy that unknown demand- it has nothing to do with people, actual immigration is not a very good predictor of house prices.

-

Speaker: House prices and the "Magic Money", in reply to

twenty four thousand stories high

It would give Epson a special character.

-

Speaker: House prices and the "Magic Money", in reply to

Well spotted, opps. I was think of the LGA (local government act) 2002., which free market types blame for red tape making house prices rise (without debt increasing at the same rate, through the power of time travelling back).